•

Expect a pause post the

December rate cut.

• Yield upside limited; investors

should add short term bonds

with every rise in yields.

•

Short term 2-5-year corporate bonds,

tactical mix of long duration Gsecs and

income plus arbitrage are best strategies to

invest in the current macro environment.

•

Selective Credits continue to

remain attractive from a risk

reward perspective given the

improving macro fundamentals.

Happy New Year from the entire team at Axis MF!

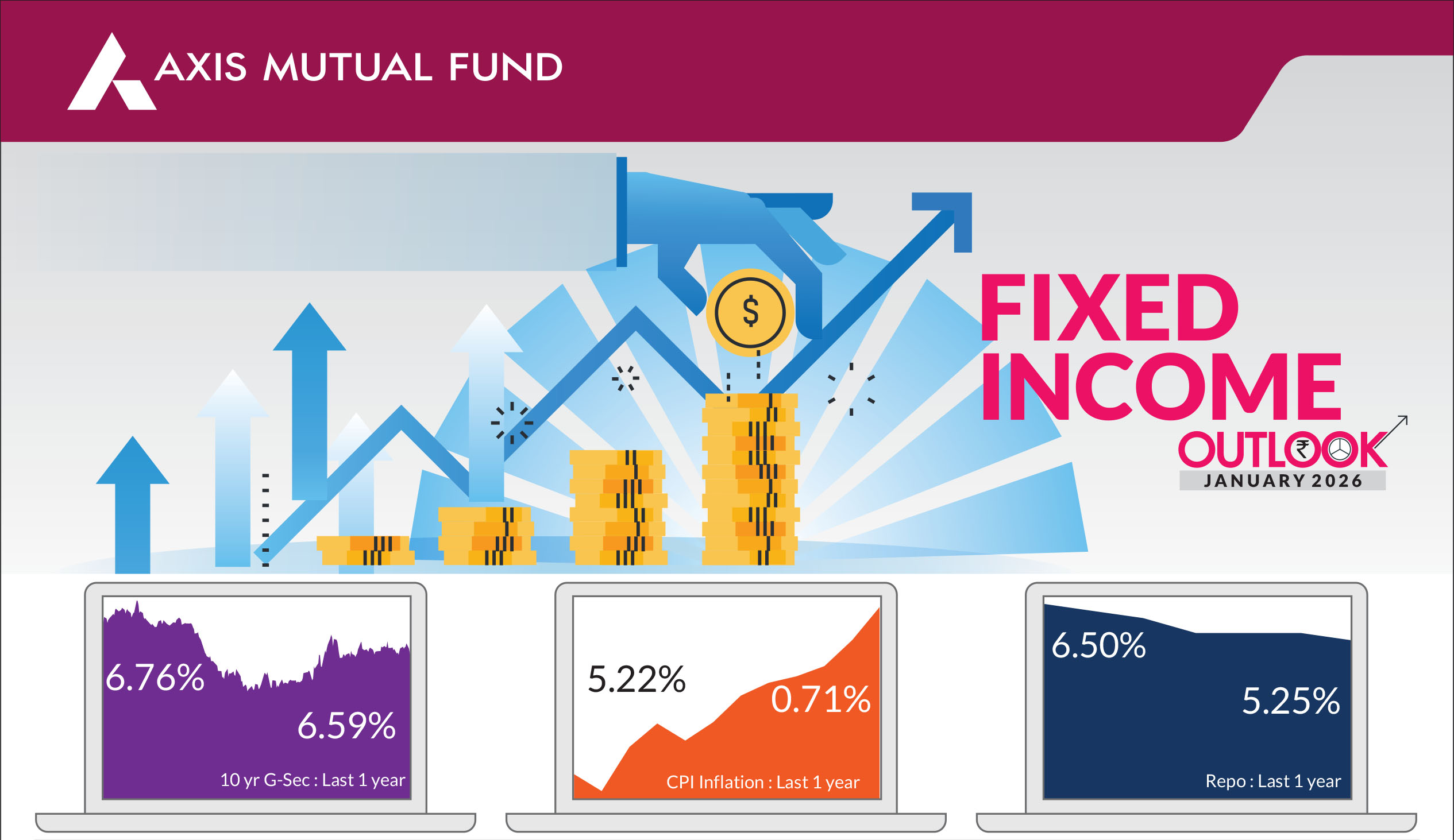

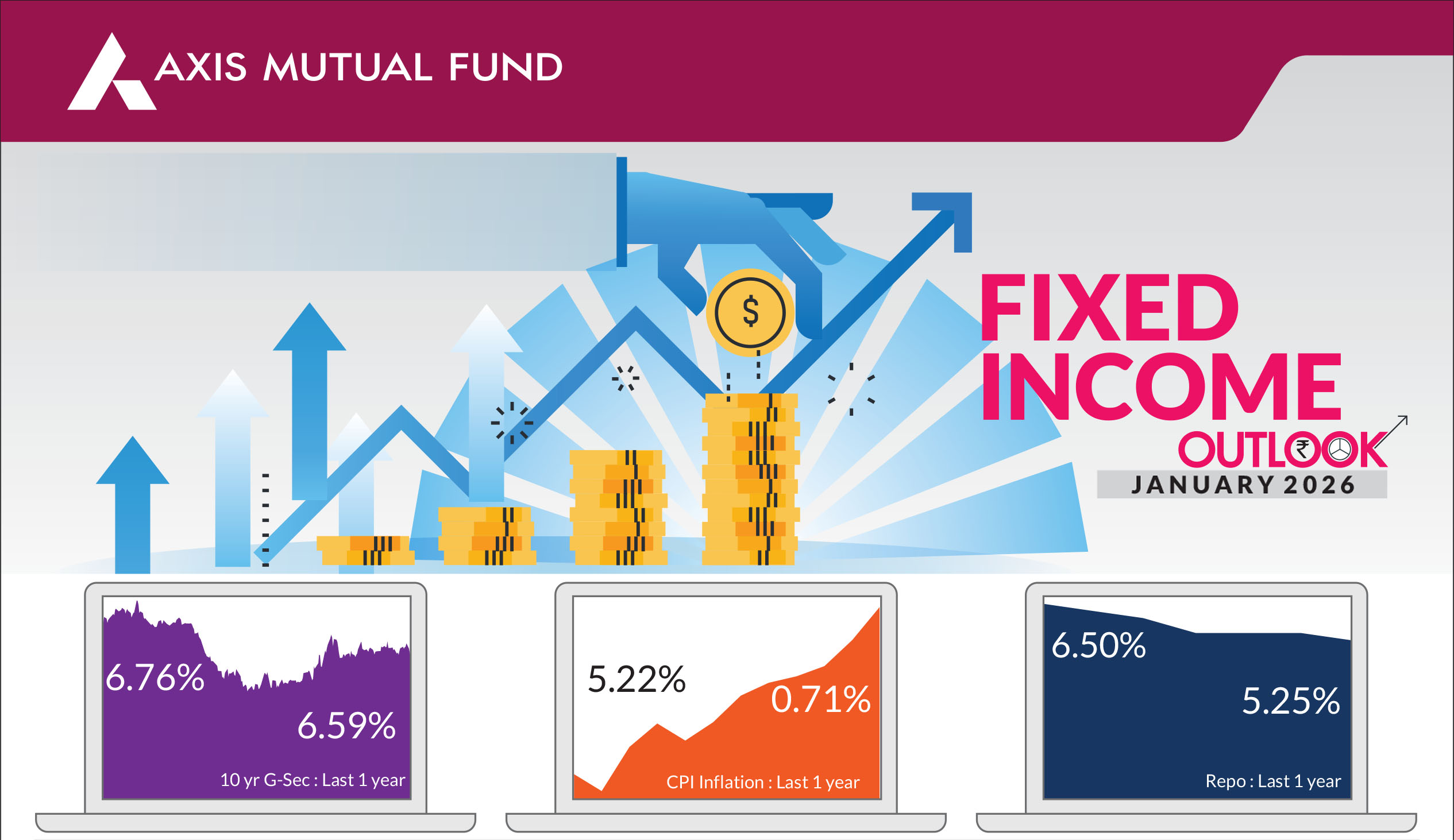

Bond yields traded higher over the month with the 10-year benchmark government bond

yield rising 10 basis points to end at 6.59%. US Treasury yields also rose, with the 10-year

yield ending the month at 4.17%.

2025 was marked by abundant liquidity and a supportive macro backdrop that fueled a

strong rally in India's debt markets. Benign CPI inflation, which fell sharply from around 5%

to as low as 0.25%-0.71%, created ample room for

monetary easing. The Reserve Bank of India (RBI)

responded with a cumulative 125 bps reduction in policy

rates and four successive CRR cuts, injecting nearly Rs

2.6 trn into the banking system. These measures,

combined with expectations of moderate GDP growth,

eased funding conditions and supported credit

transmission across sectors, reinforcing confidence in

the economic recovery. Coupled with OMOs and forex

swaps to the tune of Rs 12 trn, this easy liquidity environment kept short-term rates

suppressed even as long-term yields edged higher, anticipating the end of the rate-cut cycle.

The result was a steep yield curve across government bonds, SDLs, and corporate bonds,

creating attractive opportunities in 3-5-year corporate strategies that delivered strong

returns, while tight spreads persisted across segments.

KEY MARKET EVENTS

RBI lowers rates in December policy : the Monetary Policy Committee (MPC) of the RBI lowered interest rates by 25 bps to 5.25% and maintained a neutral stance. This decision was shaped by a "goldilocks" backdrop-robust growth and exceptionally low inflation despite a weaker currency.

Banking liquidity in positive : On December 23, the RBI announced a series of measures to

inject durable liquidity into the banking system amid FX interventions and rising yields. Key

actions include: 1) OMO Purchases of Rs 2trn in four tranches of Rs 500 billion each, scheduled

for a) December 29, 2025 b) January 05, 2026 c) January 12, 2026 and 4) January 22, 2026. In

addition, a US$10 billion, 3-year buy/sell swap has been slated for January 13, 2026.

Earlier, in its December policy meeting, the RBI had initiated liquidity infusion through OMO purchase auctions of Government of India securities worth Rs 1 lac cr, conducted in two tranches of Rs 50,000 cr each on December 11, 2025, and December 18, 2025 and a USD/INR Buy/Sell Swap auction of US$ 5 billion for a tenor of three years held on December 16, 2025.

Inflation rebounds from lows : CPI inflation rose to 0.71% in November from a record low of 0.25% in October. Inflation remains quite low due to a) weak food inflation, concentrated in vegetables, pulses and spices b) weaker core goods inflation as GST cuts are passed through. The central bank in its December monetary policy revised inflation forecasts upwards and expects inflation to stand at 0.6% in December and rise to 2% for FY26.

Meanwhile, the MoSPI will release the new CPI series based on HCES 2023-24 from Feb 2026 thus revising the CPI weights in 2026 - this would mean overall lower weight of food in the overall basket. The new basket will include price data from e-commerce platforms for retail sales, and web portals for airfares and telecom services and likely capture rents better.

US treasury yields rise : Despite the rate cut by the Fed, the yields on US Treasuries rose 15 bps. The minutes of the Fed meeting showed a highly divided committee as some policymakers argued for additional easing to prevent further softening in the labor market, while others said policy was already sufficiently accommodative and risked fueling inflation.

Earlier, in its December policy meeting, the RBI had initiated liquidity infusion through OMO purchase auctions of Government of India securities worth Rs 1 lac cr, conducted in two tranches of Rs 50,000 cr each on December 11, 2025, and December 18, 2025 and a USD/INR Buy/Sell Swap auction of US$ 5 billion for a tenor of three years held on December 16, 2025.

Inflation rebounds from lows : CPI inflation rose to 0.71% in November from a record low of 0.25% in October. Inflation remains quite low due to a) weak food inflation, concentrated in vegetables, pulses and spices b) weaker core goods inflation as GST cuts are passed through. The central bank in its December monetary policy revised inflation forecasts upwards and expects inflation to stand at 0.6% in December and rise to 2% for FY26.

Meanwhile, the MoSPI will release the new CPI series based on HCES 2023-24 from Feb 2026 thus revising the CPI weights in 2026 - this would mean overall lower weight of food in the overall basket. The new basket will include price data from e-commerce platforms for retail sales, and web portals for airfares and telecom services and likely capture rents better.

US treasury yields rise : Despite the rate cut by the Fed, the yields on US Treasuries rose 15 bps. The minutes of the Fed meeting showed a highly divided committee as some policymakers argued for additional easing to prevent further softening in the labor market, while others said policy was already sufficiently accommodative and risked fueling inflation.

Market view

Globally, disinflation has largely run its course and inflation seems close to its trough. While inflation trends across major economies could diverge in 2026, the key driver globally remains rising commodity prices. Any sustained increase in these prices could set the tone for inflation going forward. In 2025, commodities such as gold, silver and industrial metals saw notable gains, even as brent crude stayed subdued. In the US, inflation pressures are likely to remain sticky, fueled by tight labor markets, elevated wages, and persistent servicesector costs amid lingering supply constraints.The Euro area appears relatively stable, with inflation expected to hover near central bank targets. China, on the other hand, continues to face weak domestic demand and deflationary pressures in certain sectors, though inflation recently touched a two-year high. Japan, after a period of above-target inflation, is projected to maintain comparatively higher price levels.

Despite concerns that reciprocal tariffs would dampen growth, the US economy has remained strong. According to the latest IMF projections, US GDP is expected to expand by 2.1% in 2026, while Europe is forecast to grow at a healthy 1.7%. China is likely to maintain strong momentum with 5% growth and India is projected to lead with 6.2%. Against this backdrop, monetary easing may stay limited. The Fed is expected to cut rates by an additional 50 basis points in 2026, while the BoJ could raise rates by 25 basis points. Meanwhile, the European Central Bank is anticipated to hold steady, ensuring policy stability across the Eurozone.

In India, a stable interest rate cycle, sustained liquidity normalization and the anticipated inclusion of FAR securities in the Bloomberg Global Aggregate Index are likely to result in a flatter yield curve in 2026.

Alongside this, the OMO's already announced by the RBI to maintain durable liquidity would further help bridge the gap between issuance and demand, ensuring smoother absorption of supply. Long Bonds are now trading at neutral spreads over the 10-year benchmark G-Sec, with absolute yields in the 7.25-7.40% range and expectations of no rate hikes over the next 12 months, these instruments offer a compelling safety cushion for long term investors. Moreover, with the curve-flattening theme gaining traction, we expect long bonds to provide meaningful protection in the current environment.

Risks to our view: The risks to our view at this point are as below

• Fiscal Push: Large government borrowing in FY 27 could put upward pressure on yields if foreign inflows disappoint.

• Domestic Growth: Sustained weakness could prompt additional easing, might steepen the curve again.

• Non-Inclusion of FAR securities in Bloomberg: Although markets have been anticipating an inclusion of FAR securities in Bloomberg indices, a key risk would be India's inclusion getting delayed or may not occur at all.

• Currency: a larger depreciation in the rupee could have an impact

Strategy - Since February 2025, we have been steadily reducing portfolio duration, shifting away from long-duration strategies toward accrual-focused approaches. This year, we see accrual and selective tactical duration as the dominant themes, particularly in long bonds and state development loans (SDLs).

In this context, a barbell strategy emerges as the most effective approach-balancing shorttenor bonds for liquidity with long-duration bonds for tactical opportunities. Our preferred positioning includes 2-year AA-rated corporate bonds for steady accrual and long-tenor government securities for duration plays, offering a combination of consistent accrual and potential upside.

What should investors do?

• In line with our core macro view, we continue to advise short- to medium-term funds with tactical allocation of gilt funds to our clients.

Source: Bloomberg, Axis MF Research.